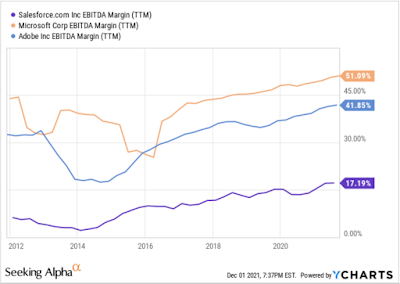

Salesforce (CRM) grew at a breakneck speed over the past two decades. The is hoping that the growth will continue in this decade.

The company's free cash flow yield is very similar to that of Microsoft (MSFT) and Adobe (ADBE). Salesforce's free cash flow yield has been consistently around the 2% level over the past decade. Microsoft and Adobe have seen their market capitalization and earnings multiple expand over the years causing their free cash flow yield to drop. I might have to look into their number more closely.

Salesforce is lagging behind Microsoft (MSFT) and Adobe (ADBE) on return on equity. Both those companies have more than 8x more return on equity than Salesforce.

Exhibit: Return on Equity

Salesforce's year-over-year quarterly revenue growth (See Exhibit: Year-over-Year Revenue Growth) has converged with Microsoft and Adobe.

Salesforce's price to earnings growth ratio (See Exhibit: Salesforce, Microsoft, and Adobe PEG Ratio) was attractive during the past decade compared to Microsoft and Adobe. If the company's growth can continue, that would justify its higher valuation multiple compared to Microsoft and Adobe. Salesforce's revenue is already in the high $20 billion, so for it to grow at a 20% rate would take some work.

Exhibit: Salesforce, Microsoft, and Adobe PEG Ratio